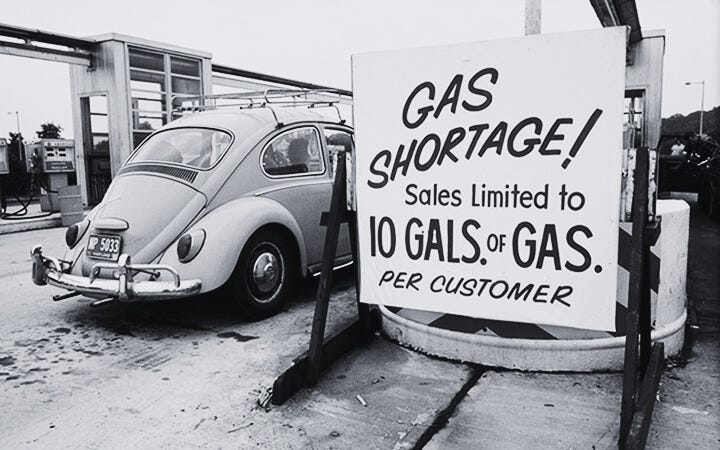

After Bretton Woods collapsed, America’s economic situation rapidly deteriorated. The move to a system of floating exchange rates saw the US dollar fall in value against the Deutsche Mark and the Yen for most of the decade. US trade and budget deficits deepened, further undermining their standing as the global hegemon. The country’s problems worsened in October 1973 when the Organisation of Arab Petroleum Exporting Countries restricted the world’s oil supplies, retaliating against nations that supported Israel during the Yom Kippur war. The US economy soon fell into recession, shrinking in size throughout 1974; inflation also spiralled upwards, reaching 11% in 1974 and 13.55% in 1980. While the economy stagnated and prices rose, the Federal Reserve raised interest rates from 9% in October 1973 to 13.60% in July 1974; unemployment also increased from 4.6% in October 1973 to 9.0% in May 1975. The stock market crashed, too, the Dow Jones Industrial Average index falling over 45% between January ‘73 and December ‘74.1

For the first time since the end of the war, the US’s economic dominance was in peril. Confronted with this crisis, Keynesian economists were at a loss for ideas. Keynesian theory said they should increase government spending to counteract the recession. But doing so would only exacerbate the price inflation that was eroding peoples’ standard of living. To curb the inflation, their theory said they should raise interest rates and cut spending—but, of course, this would only worsen the recession. Trapped between these two undesirable alternatives with the situation worsening every year, Keynesian policymakers failed to develop a coherent plan to address the crisis—a crisis caused, in part, by the deficits accrued from their ambitious social plans. The credibility of Keynes’ theories, so influential in the post-war era, was compromised.

In the 1970s, US policymakers faced an impossible task. They needed to maintain their global hegemony while running dual trade and budget deficits—by being a debtor instead of a creditor. They also needed to restart economic growth, Schumpeterian ‘creative destruction’, while controlling inflation. A solution eventually emerged—but its logic did not come from mainstream Keynesian ideas. The US government eventually achieved all these goals by developing a system Yanis Varoufakis calls ‘The Global Minotaur.’ As the world’s minotaur, the US would support the trade surpluses of other nations by voraciously importing and consuming their products. At the same time, they would develop world-leading financial technologies and practices that would encourage those nations to invest their surpluses in Wall Street banks. The banks would then ensure US dominance by loaning these funds out across the world, including to US citizens who needed credit to buy houses and fuel the consumption spending that drove this cycle.

All this would ensure capitalism’s survival. But to it, a new economic paradigm that radically diverged from Keynesianism was needed. Fortunately, one had been developing in the fringes of intellectual society since the 1930s—an economic doctrine called ‘neoliberalism.’

References

Varoufakis, Y. (2015) The Global Minotaur: America, Europe and the Future of the World Economy. London, Zed Books.

Footnotes

See https://fred.stlouisfed.org/series/UNRATE, https://fred.stlouisfed.org/series/FPCPITOTLZGUSA, https://www.macrotrends.net/2015/fed-funds-rate-historical-chart, https://fred.stlouisfed.org/series/GDPC1#0, https://fred.stlouisfed.org/series/EXJPUS, https://fred.stlouisfed.org/series/EXGEUS, and https://www.macrotrends.net/1319/dow-jones-100-year-historical-chart